All Categories

Featured

[/image][=video]

[/video]

Withdrawals from the cash worth of an IUL are normally tax-free as much as the amount of costs paid. Any type of withdrawals above this quantity may undergo taxes relying on policy structure. Traditional 401(k) contributions are made with pre-tax dollars, minimizing taxable income in the year of the contribution. Roth 401(k) payments (a strategy feature readily available in most 401(k) plans) are made with after-tax payments and after that can be accessed (incomes and all) tax-free in retirement.

Withdrawals from a Roth 401(k) are tax-free if the account has been open for at the very least 5 years and the person mores than 59. Properties taken out from a typical or Roth 401(k) before age 59 may incur a 10% charge. Not exactly The claims that IULs can be your very own financial institution are an oversimplification and can be deceiving for lots of reasons.

You may be subject to upgrading linked wellness concerns that can affect your continuous costs. With a 401(k), the cash is constantly your own, consisting of vested company matching despite whether you stop contributing. Danger and Warranties: Firstly, IUL plans, and the cash money worth, are not FDIC insured like conventional checking account.

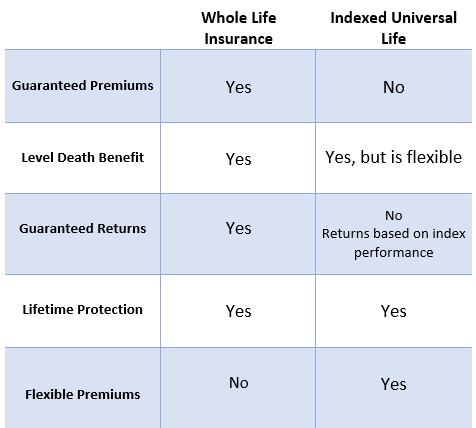

While there is normally a flooring to avoid losses, the development possibility is covered (suggesting you may not totally profit from market growths). The majority of specialists will certainly agree that these are not equivalent items. If you desire survivor benefit for your survivor and are worried your retirement cost savings will certainly not suffice, after that you may want to consider an IUL or other life insurance policy product.

Certain, the IUL can provide accessibility to a money account, however again this is not the primary purpose of the item. Whether you want or require an IUL is an extremely private question and relies on your primary economic purpose and objectives. Below we will certainly try to cover benefits and restrictions for an IUL and a 401(k), so you can even more define these items and make an extra educated choice concerning the finest method to handle retired life and taking care of your enjoyed ones after death.

Life Insurance Options With Ameriprise Financial

Funding Costs: Financings versus the policy accumulate interest and, otherwise repaid, minimize the survivor benefit that is paid to the beneficiary. Market Involvement Limitations: For many policies, financial investment development is connected to a stock exchange index, yet gains are typically capped, limiting upside potential - indexed universal life insurance versus life insurance policy. Sales Practices: These plans are often sold by insurance agents that may highlight benefits without completely describing expenses and threats

While some social networks experts recommend an IUL is a replacement item for a 401(k), it is not. These are different items with various purposes, functions, and prices. Indexed Universal Life (IUL) is a kind of irreversible life insurance policy that additionally uses a cash worth component. The cash money worth can be used for several functions including retirement financial savings, additional income, and various other financial demands.

{kind=link}

Latest Posts

Understanding Indexed Universal Life Insurance

How Does Indexed Universal Life Insurance Work

Indexed Variable Universal Life Insurance